SpaceX

What I find interesting in the SpaceX S1 filing.

SpaceX filed for an IPO today and released their S1 prospectus: https://www.sec.gov/Archives/edgar/data/1181412/000162828026036936/spaceexplorationtechnologi.htm

Beneath the flashy pictures and gaudy descriptions of interplanetary travel is, to me, an interesting future that could reach the mind-bending valuation that Elon Musk is proposing. In short, this prospectus tries to tell the story of the most tightly and fully vertically integrated autonomy, mobility, and connectivity company that could ever exist. If they purchase Tesla as is commonly believed, this could very well materialize.

But we have to ask ourselves why SpaceX is going public. The answer is typically cheap and permanent financing, which SpaceX needs a lot of. The main question we need to answer is whether all of this can succeed, because this is an all-or-nothing play. The trillion-dollar IPO they’re expected to command is a valuation of an establishment that’s profitable and stable. Being that SpaceX is quite far the opposite, anything short of continual home runs will lead to a poor future for this stock.

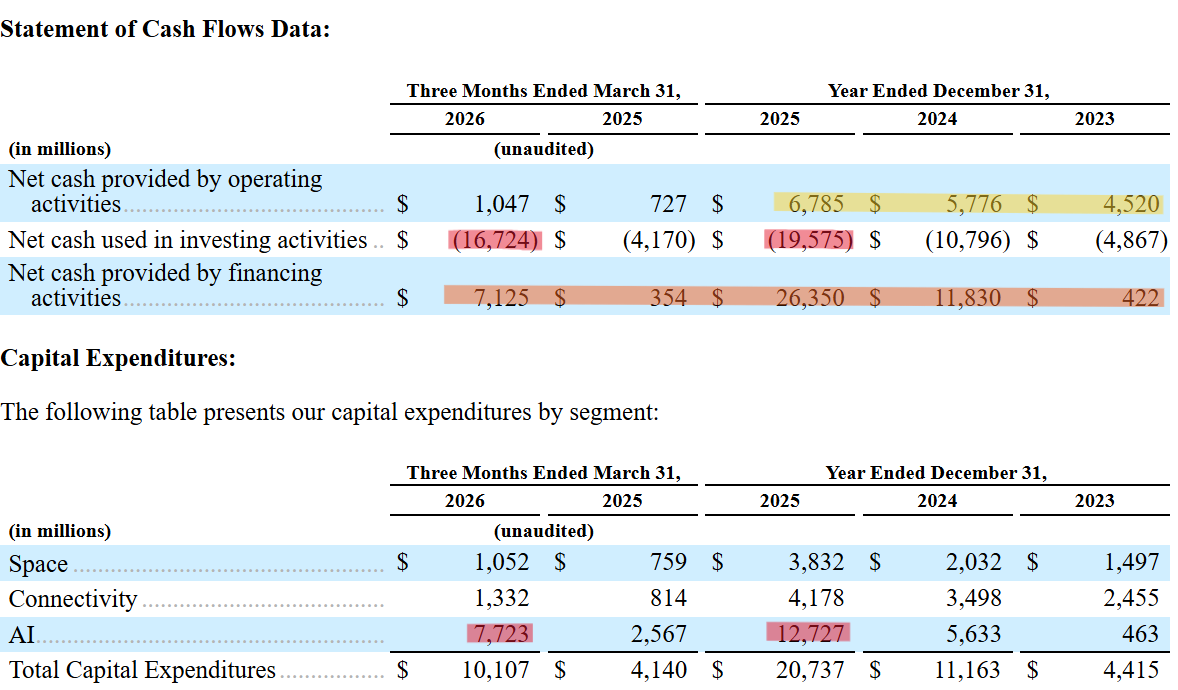

We start with an overview of their financials:

Net cash is growing and healthy - the company can make payroll, and actually makes a ton of money. However, they’re investing heavily and using outside investment to fund it. Over $26B raised in the last year, with $7B just this past quarter, is an alarmingly large amount of capital to be raising. When you sum their raises across all three companies (SpaceX, X, xAI), it reaches nearly $90B - 3-4x Uber's previous record for amount raised before IPO.

Their capex explains this when you see $12B committed to AI, with an additional $7B just in the last quarter alone. When you observe their space business (what you imagine would be the most capex-heavy segment) is burning less cash than their AI business, it shows where the business wants to go. But with $29.1B in debt, we’ll see whether the market believes it.

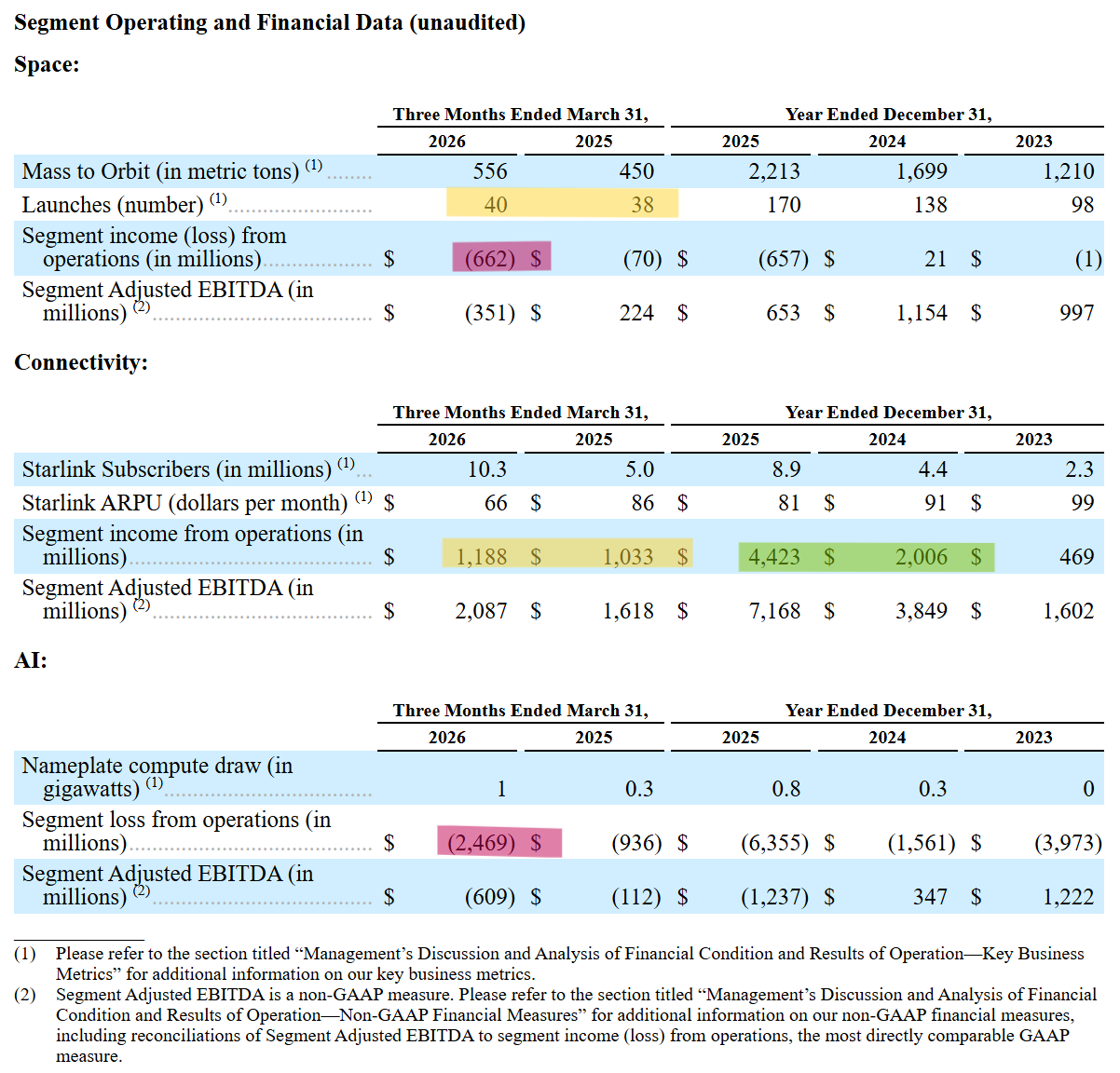

The question that every company’s valuation seems to resolve to, then, is how much we believe in the revenue growth that AI will contribute. Their segment breakdown shows us that their Starlink business, powered by the space segment, is profitable. While growth doubled from 2024 to 2025, it has stagnated with just 15% growth comparing Q1 2025 to Q1 2026. Their space business has increased launch levels, yet has experienced exponentially high losses. Their AI segment makes this company unprofitable, with the losses presumably coming from operating losses for their two data centers. Is this IPO happening because it’s the only way Elon can finance his way to compete against OpenAI and Anthropic?

The rest of the prospectus lays out some interesting key facts.

Despite the observed stagnation, the Starlink business is impressive: 10.3M Starlink subscribers in 164 countries with 99.9% uptime. They also include some key risks to growing the segment, which perhaps explains the slowing growth.

In the United States, we expect to be able to provide 5G-like connectivity to a meaningful portion of existing unmodified devices through our Starlink Mobile Gen2 service utilizing our V2 Mobile satellites, either by operating on spectrum leased to us by MNO partners or by utilizing our own domestic spectrum holdings. However, achieving full 5G NR-NTN compliance and optimal performance would likely require handset manufacturers to implement hardware and software modifications, primarily to the radio-frequency front end, in future devices.

As a result, our near-term international service strategy depends on our ability to establish MNO spectrum partnerships on a market-by-market basis, which does not require device hardware modifications but is subject to the successful negotiation and execution of commercial agreements in each jurisdiction. Until device manufacturers incorporate support for our international spectrum bands into future handsets, we will be unable to offer 5G-like direct-to-consumer service on our own international spectrum.

This appears to be a significant paradigm shift that will be required by parallel tech companies that are not incentivised to do so. If Apple begins competing in AI, it’ll become even less probable.

We do know, however, that SpaceX is also in the chips business (so maybe they’ll eventually even build the hardware components). Their partnership with Tesla and Intel to produce Tesla vehicles and robotic chips in-house starts the path to vertical integration. Of course, they mention the desire to build data centers in space, also powered by their launch capabilities and reusable rockets. These chips can also make it into their current data centers, which have allowed for their recent $1.25B/month deal with Anthropic for compute through 2029 and a $60B right to purchase Cursor in the future.

If they begin integrating Cursor and Grok, there’s potential for either an exodus or an influx of users to a competitor to Codex and Claude, which, based on the amount of training compute they have available, could be a superior product to both. This is one of my biggest questions about this prospectus, especially because of the following claim:

We estimate that our quantifiable TAM is $28.5 trillion, consisting of $370 billion in Space from space-enabled solutions; $1.6 trillion in Connectivity across $870 billion in Starlink Broadband and $740 billion in Starlink Mobile as well as additional opportunities in enterprise and government; $26.5 trillion in AI across $2.4 trillion in AI infrastructure, $760 billion in consumer subscriptions, $600 billion in digital advertising, and $22.7 trillion in enterprise applications.

$22.7T from enterprise applications in AI?

The company currently makes about 20% of 2025 revenue from govt contracts. Their existing enterprise revenue lines include connectivity for businesses and business partners (airlines, oil rigs, cruise lines), compute, an in-development agentic work platform (called Macrohard to jest with Microsoft), and advertising/subscriptions through X. Across both enterprise and consumer, connectivity accounts for about 60% of their business, space 20%, and AI 20%.

Let’s take their current enterprise revenue to be $3B (could be a big undercalculation - but for the sake of the math). To meet just 10% of their suggested enterprise TAM, these segments need to grow by 55% compounded over 15 years. To draw another comparison, AWS has ~30% marketshare over cloud infrastructure. For a similar level of market share in their addressable enterprise market in the next 10 years, they would need to grow 117% compounded annually. They also need to continue fulfilling their suggested business algorithm of expanding their launch capacity and continually finding new billion/trillion-dollar markets to disrupt with it. Even to match the revenue scale of AWS (~140B/year), it will take a 30% compounded rate of growth for 15 years (the CAGR is more realistic, but the consistency over the years certainly is doubtful).

This is where major flaws begin to appear for the future of this business.

In their consumer subscriptions segment, they calculate their TAM as follows:

We estimate our market opportunity based on the global population of individuals aged 10 and over in 2025—approximately five and a half billion according to Euromonitor—multiplied by the weighted average monthly subscription revenue of $12, resulting in an annualized market opportunity of approximately $760 billion.

Isn’t it a fallacy to calculate a TAM, on which your valuation is based, around an assumption that every single person is part of the addressable market that will purchase a Grok subscription?

Their future growth markets laughably include space tourism and travel, asteroid mining, and orbiting factories. Maybe I’ll be laughed away someday when these have all materialized, but these are hardly common, mass-market services on which to place your TAM or on which to rest your future valuation.

Some more problematic notes:

SpaceX purchases $131M in surplus Tesla Cybertrucks to artificially boost Tesla sales for 2025.

They’re paying $20B to Valor Partners, run by Antonio Gracias, who sits on the SpaceX board, for AI infrastructure…

Tesla owns ~3.8M shares in SpaceX through the residuals of a previous financing deal where Tesla owned xAI shares.

Both Terafab (the Intel/Tesla partnership) and Macrohard (the software initiative in xAI) are outlined as no-IP, early-stage projects.

From all of this, what we get is a fantastic satellite internet business that’s taking a very expensive foray into AI. This entire bet depends on whether you expect the world population and its companies to spend that much on AI over the next 10-25 years, and that SpaceX (whatever this company turns into) will be at the forefront of it. If the former vision comes true, SpaceX is positioned early on in this race to integrate connectivity, consumer apps, enterprise capabilities, models, compute, and potentially chips and enterprise software.

If you’re not bought in on another Elon Musk grand slam or won’t be able to stomach years of uncertainty, I wouldn’t do it. But they all said the same thing about Tesla, a stock that also struggled with years of volatility before maturing, given that it was just a car company. This is a behemoth of debt and obligations based on a precarious assumption about the rapid (paid) proliferation of a technology that changes the fabric of humanity. Where do you place your bet for the future?