Oil

A brief overview and history on trading oil futures.

For its place as the keystone of the global capitalist economy, oil doesn’t really follow many capitalist rules. Its supply can be manipulated, the entire industry in some countries is owned by sovereign governments, and a high barrier to entry means there is no real semblance of free market competition. Oil futures, the tradeable contracts that price a barrel of oil each month, are constantly reacting to these dynamics in relation to demand. Futures contracts extend out several years, but every subsequent month’s contracts are priced simultaneously.

Unlike stock options, which are derivatives that allow traders to granularly speculate on a stock, futures were made for buyers and producers of commodities to hedge against pricing risk. Before oil was in the picture, the top commodity being bought and sold was grain. The invention of the steam-powered grain elevator (safe storage for wheat so it doesn’t rot) would enable year-round storage and the promise of future deliveries using the first futures contracts. Futures immediately solved both extreme price gluts when supply would dump into the market every summer and high volatility when grain ran out in the winter. These contracts were the first time farmers could enter into a binding agreement to sell their commodity for a set price in the future, and buyers couldn’t back out to go buy it for cheaper when the expiration came. A market that began as a way for farmers to guarantee payment in the winter now tracks everything from chicken feet production to weather.

Today, oil futures are used as financial instruments for investors and oil price-dependent entities that need to hedge against price volatility. First, anyone purchasing an oil futures contract is required to put up to 10% as margin or pay the cost of 1000 barrels at the current futures price for the given strike. Profit and loss are calculated daily, meaning any gains or losses happen in real-time, not upon exiting the trade. An airline might purchase crude oil or jet fuel futures if they expect prices to go up; the gains from the futures subsidizes their added fuel costs. Similarly, if an oil producer expects prices to go down, they’ll sell oil futures to lock in a higher price before they can produce and sell the barrel. Therefore, the price of oil futures is dominated by a collective uncertainty and attempted predictions about the true change in the price of oil between now and the expiration. This is an important distinction from options, where investor sentiment is tightly coupled to narrow metrics of company performance and earnings.

Core to this pricing tension that requires all of this hedging is OPEC, a group of the largest oil-producing countries in the world that together own ~80% of proven oil reserves and coordinate to rapidly scale up or down production. This level of supply manipulation has historically been used to keep prices at high margin levels, most notably after the demand crash and rebound of the COVID pandemic. The loss of independent suppliers during the crash in demand allowed OPEC to only gradually increase production while the world fully reopened its demand. Oil companies have thus enjoyed their highest profits ever. When the fundamental pricing mechanism is not determined by the free market, investors are often trying to make future predictions on an insider game that can change overnight with one headline decision by OPEC. I’m not suggesting anything illegal - but remember, it’s only legal because the majority of the supply says so.

The best way to actually exemplify how all of these forces come together practically is to compare oil prices versus supply leading up to and immediately following the start of the war between the US and Iran in 2026. An 8% contraction in supply led to a 60% jump in the price per barrel. What we saw leading up to the attack was several geopolitical events in the region - the bombing of Iranian nuclear sites, then bombs exchanged between ships, then drone attacks - all of which weren’t taken as signs of an impending full-scale conflict, and oil prices remained flat. Once the full-scale war was initiated, though, the reaction was severe and swift as traders bought oil futures to speculate against price spikes. The futures were being priced based on the worst-case collective fear of traders, not so much the actual and immediate impact on supply.

With the mechanics of how to trade oil understood, we can better understand what exactly we’re trading. First, the canonical oil in a futures contract is crude oil - the source, raw hydrocarbons that are taken out of the ground. Futures exist for any other oil derivative, though, including jet fuel and gasoline, and investors can purchase options on these futures for more granular strikes.

There are two methods of extraction depending on what sits between you and the oil. Softer rock can be directly drilled conventionally and uses the Earth’s natural pressure to push oil out of reservoirs and up through well bores. Harder rock needs to be fractured and uses water pumped into the rock to force the oil out. Depending on the geographic location, two types of crude can be produced using either method - sweet crude with <0.5% sulfur content and sour crude with >1% sulfur content.

The smoother, sweet crude is easier and cheaper to refine, meaning it sells at a 5-10% premium to sour crude, which requires additional processes to remove the sulfur impurities. Oil produced in the US (called West Texas Intermediate), the North Sea (Brent), Malaysia, Australia, and North/West Africa is majority sweet crude (approx. 60% of US oil exports are sweet crude). Regions that produce sour crude include the Middle East, South America, Canada, and the Gulf of Mexico (which is why we have oil pipelines from Canada to Louisiana, where US refineries are concentrated).

This split has prehistoric roots. When the planet was covered in volcanoes, sulfur gas was being pumped into the sky and interacting with oxygen, which was newly introduced to the atmosphere en masse by photosynthesis. This reaction would result in sulfur rain that landed in the oceans and created mass sulfur deposits across the ocean floors. As the land mass shifted and major sections of ocean became isolated lakes, the marine life in them started to die. The lack of oxygen from the larger sea current would create dead zones of marine life, now mixing with the sulfur and microbes that remained. Crucially, in areas with high iron content in the ground, the sulfur was stripped away and converted into pyrite before it had a chance to embed into the decomposing, organic material. Without the presence of iron, the microbes would bind the sulfates to the old plants and life as it used the oxygen in that organic material to survive. The microbes would additionally release hydrogen sulfide gas as a byproduct of their decomposition. As all of this material became compressed over the next millennia, the sulfur-containing material would turn into the muddy, sour crude, while the stripped, clean material would become the easily extractable sweet crude.

Next, once we have the crude, what happens, and how do the requirements (and price implications) continue to diverge between the two types?

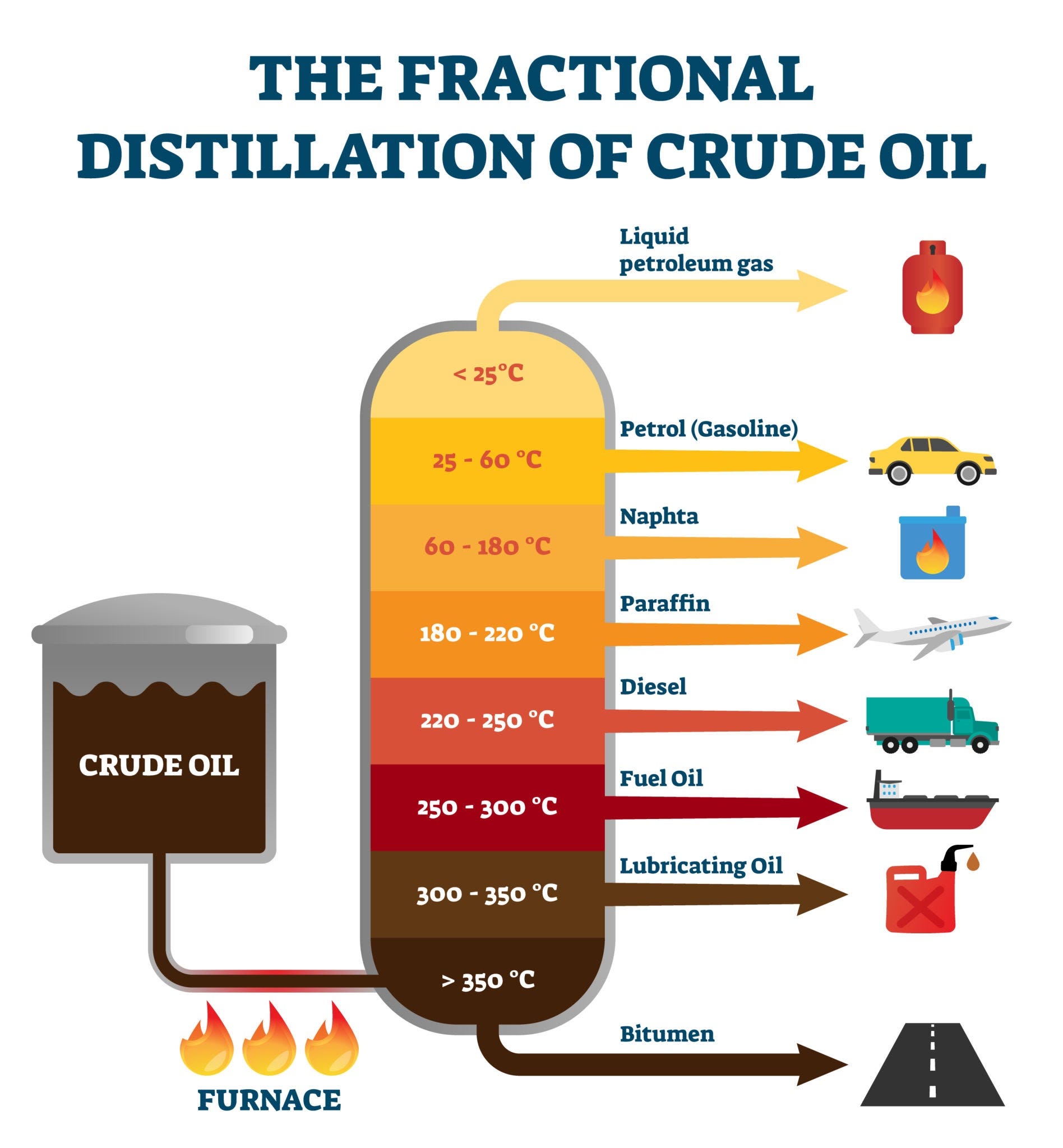

After extraction, the crude needs to be transported, refined, transported again, stored, processed, and delivered for consumption. Below displays the refinement process in particular, which is where the different byproducts of heating crude are produced.

Sweet and sour crude differ in how they can be transported, refined, and stored, and cannot be mixed. Sour crude with its high sulfate and hydrogen sulfide gas content is highly volatile upon extraction. First requirement of sour crude extraction platforms is to have an on-site stabilization tower that gently heats the crude and burns of this gas. In transport, pipelines and containers must use highly durable steel and avoid any moisture. A lapse in either could result in the worst case, where sulfur in the crude, any remaining sulfide gas, and hydrogen atoms can bond to push themselves physically through gaps in steel grains. This makes the steel brittle and prone to pipeline breaks. While sweet crude does not require any of this for transport, it has its own caveat in refinement.

Once the crude has been extracted and transported, it must now be loaded for delivery to a refinery. This is an interesting area to observe since pipeline or transport capacity doesn’t always match terminal loading capacity, where bottlenecks can be seen at some pipeline endpoints. At the refinery, it is then heated to 750F to distill it into the component parts. Of course, sour and sweet crude require completely different refineries, with the sour refineries having to conform to the same material and safety standards as in transport. Sweet crude, though, being lighter, at this point requires larger distillation towers than sour, since a larger volume of heavy vapors is released during distillation. An additional step after the above graphic strips out any additional sulfur, removes impurities, and re-applies intense heat to the bitumen layer to extract any last products.

Finally, these products are delivered to storage terminals, typically outside large metro areas. Here, companies like Shell and Chevron will blend additives before final delivery to a gas station or airport. After all is said and done, 59% of the end cost comes from the barrel of oil, 18% from refining, 12% from distribution, and 11% from taxes (unless you’re in California, where you get a 16% tax, environmental laws requiring higher grade, and the mountains preventing pipelines, requiring expensive international shipments, all contributing to the single highest consumption prices for crude oil products).

Now, at this point, you may be honing in on two facts: the US produces sweet crude but is also a net exporter of oil. Shouldn’t we be retaining and refining our domestically produced oil?

The final history lesson of this piece takes us to the start of the oil boom when sweet crude was first found in Pennsylvania in 1859. Production in the early days was negligible by modern standards, but sweet crude extraction would continue to proliferate across the US until reaching a peak of 10 million barrels per day in 1970, when the availability of conventionally extractable oil began to decline. In the 1950s, oil discoveries in the Middle East would cause global production to skyrocket to 50 million barrels per day by 1970.

The world was awash with cheap but sour crude oil from the Middle East, and the United States, who quickly becoming the biggest buyer of it, needed capacity to refine more of it. Between the 1970s and 1990s, American oil companies built generational infrastructure to refine sour crude oil on-shore and would lead to ever-increasing levels of oil imports that the US relied on to operate its society. The completion of sour refining capacity happens around the same time US oil production begins a long slide to nearly half its production over the next 15 years.

Then, as a saving grace for the US industry in 2008, fracking proved able to extract oil from tight shale rock formations that had previously been inaccessible. US oil production would reverse back above 10 million barrels per day over the next 6 years, and we would become a net exporter for the first time. However, since 2005, refinery construction has been hampered by environmental regulation, and the cost to retrofit a refinery for either sour or sweet throughput is placed on the order of $500m-$1b.

The staggered discovery of oil reserves and technology, plus an all-in construction boom for sour crude refineries, would make our refinery capacity inflexible to domestic sweet crude production, which now remains what the US produces the most of.

Out of this has come a global balancing act that appears to be working well (perhaps because it just has to). The US produces sweet crude that it can’t refine, so it sells it to European and Middle Eastern countries to refine and use domestically. They then purchase back the same amount of sour crude at a 5-10% discount, utilize now established and low-cost refineries, and deliver it to American consumers. This “subsidy” in part enables US drillers to have a breakeven point of approx $65 per barrel, while this sits around $80-90 for most Middle Eastern countries.

Looking forward from today, the future of oil is accepted to be finite. Producers like Shell are claiming they reached peak oil production in 2019, a morbid concession for a company profiting around $20B a year off of oil and gas. It appears many companies across the board in oil and gas share this sentiment, with capital expenditures down to record lows in recent years - oil companies are reaping profits and returning on investment while they can and have stopped pricing their own shares for the future.

Now, oil production won’t go away overnight or over the course of even years. I expect current downturns in production to sustain themselves, partially recover with better technology, before reaching a true decline that reflects the end of our global reserves. But you know what, we’re going to find another reserve, and then another, and then another, such that oil will remain dominant at least for our lifetimes. The question is how quickly and proactively alternatives begin to fill the need for dense, reliable energy sources that power our societal fabric.

Sources

https://www.weforum.org/stories/2022/11/oil-opec-energy-price/

https://www.cmegroup.com/markets/energy/crude-oil/light-sweet-crude.margins.html

https://www.cmegroup.com/education/courses/introduction-to-futures/margin-know-what-is-needed

https://www.acs.org/education/whatischemistry/landmarks/pennsylvaniaoilindustry.html

https://pubs.geoscienceworld.org/aapg/aapgbull/article/107/6/851/623376/

https://www.strausscenter.org/energy-and-security-project/peak-oil/

https://www.statista.com/statistics/748207/breakeven-prices-for-us-oil-producers-by-oilfield/

https://vision2030.ai/encyclopedia/oil-price-impact-saudi-economy/

https://www.cnn.com/2021/02/11/business/shell-oil-production-peak/index.html

https://www.ecowatch.com/shell-oil-production-peak-2650478989.html

https://www.eia.gov/energyexplained/gasoline/factors-affecting-gasoline-prices.php

https://usafacts.org/articles/how-much-do-you-pay-in-gas-taxes/

https://www.energy.ca.gov/estimated-gasoline-price-breakdown-and-margins